Introduction

Founders sometimes establish a lockup on the tokens that starts after they are generated/distributed in order to align incentives because tokens are noticeably much more liquid than traditional equities. These detentions may last for a few hours or for many years. By examining where lockups are now and how they’ve developed over the previous few years, we’ll be discussing industry norms below.

Founders sometimes establish a lockup on the tokens that starts after they are generated/distributed in order to align incentives because tokens are noticeably much more liquid than traditional equities. These detentions may last for a few hours or for many years. By examining where lockups are now and how they’ve developed over the previous few years, we’ll be discussing industry norms below.

Vesting Types

There are two distinct themes—time-based and trigger-based—that can be used to characterize vesting schedules. An agreed-upon date, such as the day an agreement is completed or a specific time after it is executed, is when a time-based vest (including the cliff) starts. Following a certain event, a trigger-based vesting schedule is initiated. This often comprises a token creation event, but it might also entail the launch of a mainnet or the placement of a project token on a well-known exchange. According to Lauren Stephanian, “70% of token vesting schedules were trigger-based and of those, 65% began after a token generation event.”

Vesting Period

Vested times for the trades under analysis ranged from individual blocks to monthly, quarterly, and semi-annually. Unexpectedly, a significant fraction of these transactions vest block-by-block, which is a relatively recent trend, but the majority – more than a third – vest monthly.

Cliffs & Locking

A cliff is the time before any token distribution occurs. In the crypto world, cliff lengths might be anything from nonexistent to more than a year. In 2018, one-year cliffs in vesting schedules were relatively widespread; at the time, terms were frequently verbal or handshake agreements, but they were not formally recorded. For two reasons, these one-year cliffs were well-liked: Rule 144 and the Effects of SEC v. Telegram.

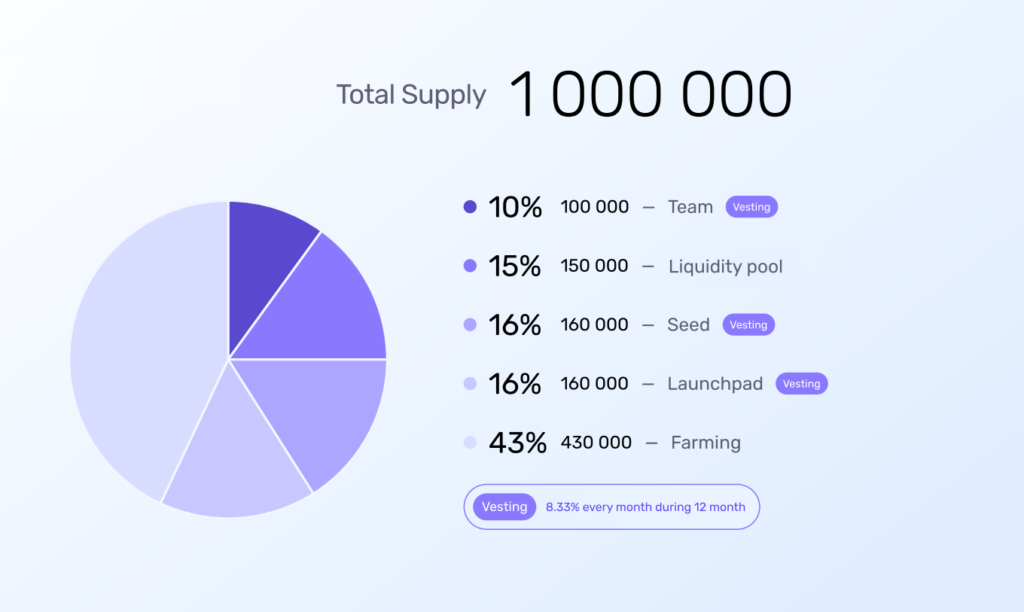

Average vesting schedule

In 2022 the following schedules made the average

Cliff: 0.65 years

Vesting Length: 2.3 years

Does an Ideal Vesting Structure exist?

The term “Ideal” is used to refer to a vesting schedule that has the least detrimental effects on token prices at each vesting date and the least fluctuation for token prices overall. Examining a number of tokens to test the following hypothesis for both linear vests (where the token starts vesting at the cliff and then vests every block over a certain amount of time) and particular date vests (when there are specified dates when the token is released):

Comparing linear vesting to vesting on a specified date Hypothesis A: Over the course of the vesting term, linear vests are more volatile than particular date vests. Hypothesis B: Compared to linear vests, specific date vests have a negative effect on token price at first unlock.

Comparing specific date vests

Hypothesis C: Because of the foresight into probable token dumping, a greater percentage of tokens freed at the cliff has less influence on token price.

Hypothesis D: Projects with more periods of unlocking and fewer total vesting dates as a result have superior maximum drawdowns than those with fewer periods of unlocking and more total vesting dates.

Hypothesis E: Tokens with shorter total lockups have less of an influence on prices than projects with longer total lockups.

These were the outcomes:

- Shorter total lockup durations, greater unlocks, and gaps between unlock that are longer (up to 6 months) produce better “worst returns” than intervals that are shorter.

- Compared to particular date vesting plans, linear vesting schedules are less volatile during the vesting term.

- 6-month cliffs are better over 1-year cliffs, or none at all, for precise date vests.

- Greater initial unlocks than smaller first unlocks have less of an adverse pricing impact.

- Additionally, linear vests outperformed particular date vests in terms of their influence on pricing after the first unlock event.

We advise founders who choose particular date vests over linear vests to do so on the basis of solid research, and founders who still want specific date vests may take these conclusions into account when choosing their vesting structure.